How does retirement work? Your complete guide from A to Z

How does retirement work? After several changes due to the Pension Reform, it's common to have questions. Understand all the information and changes!

Advertisements

THE retirement public security is available through the Social Security system, which is funded by three parties: employers (companies), workers (private sector employees, public servants and self-employed workers) and the Federal Government.

Thus, in the case of the Government, the amount is collected through taxes.

In this way, several benefits are offered through the system, including retirement and its different types, which we will clarify throughout the content.

Summary with the topics presented

- What is retirement in Brazil and how does it work?

- Retirement by age from A to Z;

- Who is entitled to retirement by age?

- What is the retirement age?

- How does retirement by age work for those who have never contributed?

- New rules in 2022 – see what has changed in retirement by age;

- Retirement age table;

- Retirement by age, calculation: how to do it?

- Special Retirement from A to Z;

- What is special retirement?

- How many years does one retire on special retirement?

- Who is entitled to special retirement?

- How does early retirement work? See the new rules

- Special retirement simulation: where to do it?

- Table of special retirement professions;

- Disability Retirement from A to Z;

- What is disability retirement?

- Who is entitled to disability retirement?

- Disability retirement requirements;

- Disability retirement due to illness;

- Can disability retirement be canceled?

- Retirement by contribution time from A to Z;

- What is retirement based on length of service and how does it work?

- Why did retirement based on length of service end?

- How do transition rules work?

- Transition rules – Toll 100%;

- Frequently asked questions;

- Retirement as an MEI, how does it work?

- When does a retiree have to provide proof of life?

- How can a retiree withdraw their FGTS?

- When does a retiree receive his thirteenth salary?

- Is retirement exempt from income tax?

- How does retirement work for those who have never worked?

- How does retirement work for those with low income?

- How does single contribution retirement work?

- Conclusion.

What is retirement in Brazil and how does it work?

The Social Security system can also be seen as an insurance in which the employee participates through monthly contributions.

As an advantage, the worker is guaranteed an income to be used when he can no longer work, that is, when he retires.

Therefore, it is a system that guarantees your retirement, in addition to the right to other types of benefits such as maternity pay, sickness benefit and survivor's pension.

Therefore, it is insurance that protects workers against economic risks, including loss of income due to illness or disability.

Retirement by age from A to Z

This type of benefit is only offered to Brazilians who have reached a certain age range.

So, this is the insurance with the most relaxed requirements, it is the most sought-after option by Brazilians.

Also due to this characteristic, it was the type of retirement that underwent major changes with the Pension Reform.

Who is entitled to retirement by age?

The Social Security Regime (RGPS) lists insured persons into two groups, which, in turn, are divided according to the type of worker.

In this sense, the following are entitled to retirement by age: mandatory insured persons and optional insured persons.

Firstly, it fits into the category of mandatory insured the individual who is compulsorily registered with Social Security, whether he or she is a worker or not.

Within this category, it is worth highlighting the 5 types of workers: domestic worker, employee, individual contributor, special insured and casual worker.

In the case of the special insured, understand that it would be the individual who carries out fishing, crafts, production or rubber tapper activities.

Secondly, there is the group of optional insured, the individual who decides to contribute to Social Security on his own.

This way, the contribution is made manually and monthly.

Therefore, one of the requirements is to be over 16 years old, in addition to not being a mandatory insured person.

Within this group, we can highlight: housewife, student, unpaid condominium manager, individual who is no longer a mandatory social security insured, intern, scholarship holder and Brazilian resident or domiciled abroad.

The group also includes prisoners who do not carry out paid work, insured individuals held in closed or semi-open prisons who work for one or more companies or work with handicrafts on their own.

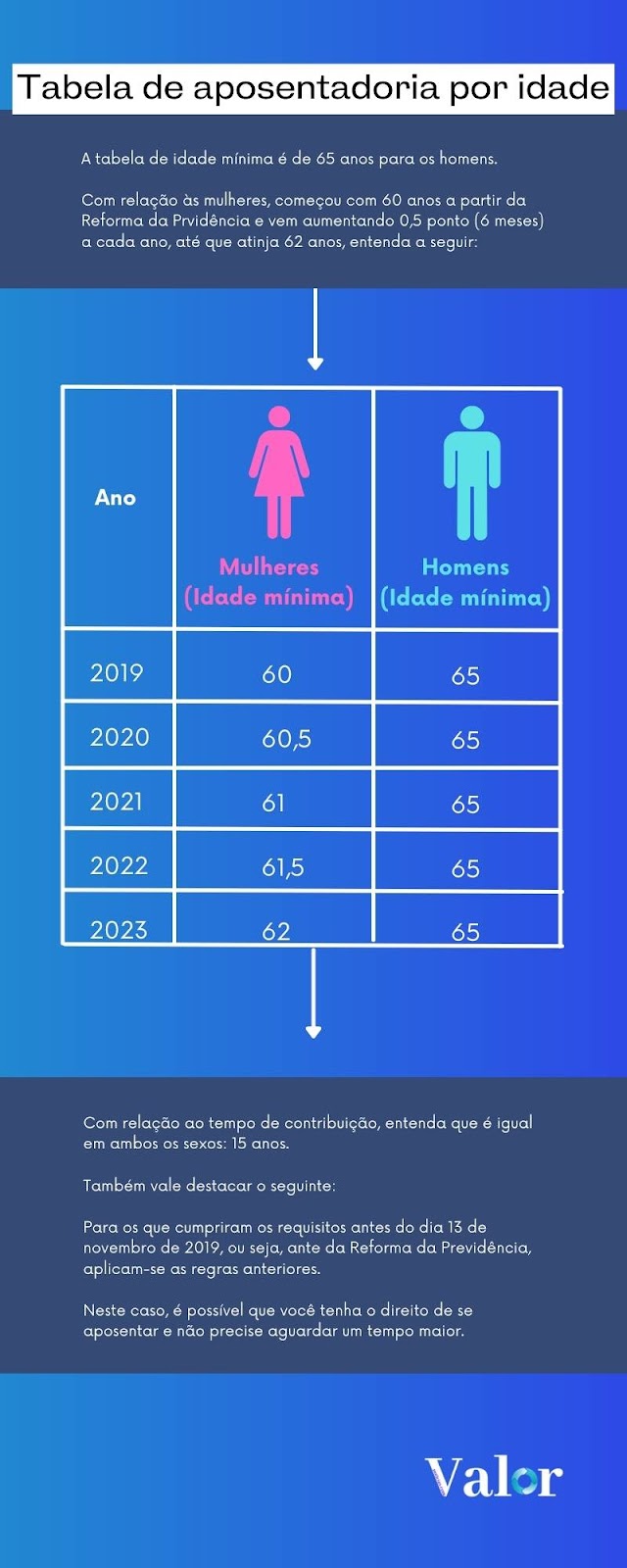

What is the retirement age?

If you worked before the Pension Reform came into effect in 2019, you can retire at 65 if you are a man and 60 if you are a woman.

Therefore, in both cases, the contribution period is 15 years.

Therefore, the rule is valid for those who completed the requirements until 11/12/2019.

On the other hand, for those who did not meet the requirements to retire by age before the start of the reform, although they started working before it, the Transition Rule is applied:

In other words, to be entitled, the man must be 65 years old and have contributed for 15 years.

In the case of women, they are required to be 60 years old + 6 months per year, starting in 2020, reaching 62 the next year, as well as 15 years of contributions.

As for male workers who started working after the reform, they need to be 65 years old and have contributed for 20 years.

In other words, for women, the contribution remains at 15 years, but retirement is only received at 62 years of age.

However, it is worth highlighting the special cases in which some conditions change:

Rural workers, indigenous people, extractivists (rubber tappers) and artisanal fishermen also have the right to retirement by age.

Therefore, the minimum age to receive retirement benefits has decreased: 60 years for men and 55 for women, requiring contributions for 15 years.

How does retirement by age work for those who have never contributed?

As mentioned above, whatever your profile, you must contribute for at least 15 years to retire by age, as this is an insurance policy.

For a person to retire without having contributed, they are placed under another type of benefit that is no longer considered retirement.

In the topic “How does retirement work for those who have never worked?”, we provide more information on the subject.

New rules in 2022 – see what has changed in retirement by age

Note that through the transition rule, 6 months have been added each year for women, until they reach the age of 62 in the year 2023.

Previously, the minimum age was 60 years, increasing to 60 and a half years in January 2020.

Starting in 2021, the minimum retirement age for women increased to 61. It will now be 61 and a half in 2022.

And since 2019, the minimum age for men is 65.

Retirement age table

Retirement by age, calculation: how to do it?

Before the reform, the calculation was done like this:

The insured had the possibility of excluding the lowest 20% contributions.

Therefore, with the sum of the 80% highest contribution salaries and their average, the coefficient was applied.

Thus, the coefficient was based on multiplying the average value by 70%, plus 1% for each year contributed:

This type of calculation was applied to people who met the retirement requirements before November 13, 2019 (when the reform took place).

Therefore, it includes those who have not yet requested the benefit or are awaiting a response to their request, having met the requirements.

On the other hand, it is worth highlighting how the calculation is done after the reform:

It is no longer possible to exclude the 20% smaller contributions, that is, 100% of contribution salaries after 1994 will be used.

After adding, the value is divided by the number of months used.

On average, a different coefficient is applied than the previous calculation, starting at 60%, and men earn 2% more for each year contributed after 20 years and women after 15 years.

Since this is not a simple calculation, we recommend that you use the Cálculo Jurídico social security factor calculator.

Just click at this link, tap “start” and enter the calculation date, date of birth, gender, as well as the contribution time, including years, months and days.

Special Retirement from A to Z

Furthermore, we must mention the INSS benefit aimed at workers:

What is special retirement?

Due to the conditions of their profession, individuals who have been exposed to unhealthy conditions are entitled to this type of retirement.

In case you didn't know, unhealthy activities expose employees to agents that are harmful to health, whether biological, physical or chemical.

An unhealthy activity also puts the worker at risk of death, as he is exposed to danger.

How many years does one retire on special retirement?

The answer may vary depending on the type of activity performed by the professional, given that some agents are more aggressive and serious than others.

That is, the more harmful the agent, the shorter the time for the employee to retire.

Therefore, Underground mine workers retire after 15 years of contributions, since the degree of danger is maximum.

As a moderate degree and granting retirement in 20 years, it canWe highlight the above-ground mine workers who are exposed to asbestos.

Finally, there is the minimum level that guarantees retirement after 25 years of contributions, including the remainder as electricians, security guards, workers subject to noise above the law, intense cold or heat, among others.

Who is entitled to special retirement?

Until 1995, the law clarified the professions included in special retirement, something that continues to be valid with the reform.

In other words, for those who worked until 1995 in one of the professions, the right to special retirement is guaranteed.

However, if your professional activity does not fit into the list, even though it is unhealthy or dangerous, you can recognize the special activity in order to be entitled to the benefit.

Generally the employee's Professional Social Security Profile (PPP), and the most commonly used document to prove a special activity.

This is a document structured by the occupational safety engineer or occupational physician, in accordance with the Technical Report on Environmental Conditions at Work, LTCAT.

Therefore, the PPP certifies exposure to harmful agents, in addition to proving that the effects cannot be neutralized through the use of protective equipment.

How does early retirement work? See the new rules

Through the reform, employees who begin their professional activity after 2019 must meet two main requirements: contribution time and a minimum age.

In this sense, we have the following scenario:

- For those who work in underground mines, the contribution is 15 years and the minimum would be 55 years to retire;

- For employees who have contact with asbestos, the contribution is 20 years and retirement comes at 58 years of age;

- With the requirement of 25 years of contribution and a minimum age of 60, it is also worth highlighting individuals who carry out activities in which they must deal with agents that are harmful to health.

Note: before the reform, the minimum age was not required, so the main requirement was the contribution period.

That is, a professional who started working at the age of 25 in 2020 in a job with noise levels above the permitted level without interruptions can only retire at the age of 60.

In other words, you must wait another 10 years to be entitled to retirement.

Special retirement simulation: where to do it?

The INSS itself has a simulator that can be accessed through the “Meu INSS” platform, although it is essential to have certain care.

Since the simulation is performed using information from the INSS database and the information you provide, make sure the period is recognized as special.

Also, check that all periods you worked are recorded in the social security system.

This way, if you notice any inconsistency, simply request correction or acknowledgement.

As for the simulation, log in to the “Meu INSS” platform and select the “what do you need?” option.

After that, write “simulate retirement”.

If necessary, check your details and change them in pencil, such as your date of birth or your social ties.

So, just click on “recalculate” to check two options: “request retirement” or “download PDF”.

The second is a good alternative for those who want to check contribution data in detail, either alone or with the help of a professional.

It is also worth noting that the simulator result serves as a consultation on the time contributed, and is not decisive in achieving retirement.

As a result, the INSS simulator does not clarify which rule is best in your case or how to obtain documents that prove the special contribution period.

The platform may also display errors regarding contribution time that is not in the system, so stay tuned!

Table of special retirement professions

The tables can be divided according to the risk of the activity, check it out:

First, let's talk about high-risk activities, where the contribution is only 15 years:

| Cave Rock Driller | Digger |

| Rock Carrier | Underground rock crusher operator |

| Miners underground | Shocker |

| Crusher |

In the case of activities with medium risk and a 20-year contribution, we can highlight the following professions:

| White Phosphorus Extractor | Paint Manufacturer |

| Permanent workers in underground locations, away from the work fronts | Explosives Charger |

| White Phosphorus Extractor | Mercury Extractor |

| Lead Rolling Mill | Lead Molder |

| Worker in Tunnel or Flooded Gallery | Fire Chief |

| Lead Smelter |

Finally, we can talk about the professions with the lowest risk and a contribution period of 25 years:

| Industrial chemists, toxicologists | Chemical, metallurgical and mining engineers | Assistants or General Services who work in unhealthy conditions |

| Diver | Bus driver | Radioactivity Technician. Receptionist (Telephone Operator) |

| Truck Driver (over 4000 tons) | Surgeon | Technician in analysis laboratories and chemical laboratories |

| Tractor Driver (Large); Boiler Operator | Train Driver | Urban and road transport |

| Welder | Graphic Cutter | Dyeing Assistant |

| Cold Room Operator | Airline | Spray Painter |

| Mechanical Lathe Operator | Airline Runway Service Officer | Construction Worker |

| Dyer | X-ray Operator | Fishermen |

| Dentist | Nurse | Diver |

| Stoker | Oil extraction workers | |

| Graphic | Journalist | Driller |

| Nursing Assistant | Doctor | Electrician (above 250 volts) |

| Fireman | Metallurgical | |

| Stevedore | Teacher | Surface miners |

| Security guard (armed or not) | Rail transport | Supervisors and Inspectors of areas with an unhealthy environment |

Disability Retirement from A to Z

On the other hand, this benefit is offered to workers who are permanently unable to perform their work activities, we will understand more below:

What is disability retirement?

Firstly, it is essential that your incapacity and impossibility of rehabilitation be proven through the INSS medical examination.

Therefore, a reassessment will be carried out after two years to prove the incapacity and maintain the benefit.

It is worth noting that the disabling illness or accident does not need to have occurred during work for the person to be eligible for the benefit.

That is, if you have a genetic disease or suffered an accident outside of work hours, you will be entitled to this type of retirement, if you meet the requirements.

It is also important to highlight that the disability retirement differs from sickness benefit or temporary disability benefit.

The name of the benefit itself indicates that the person's disability is temporary, so they receive the amount for a period of time until they recover and return to work.

Therefore, we have content in which we clarify all the details about the aid, to find out more, access here.

Who is entitled to disability retirement?

Therefore, in order to bring greater clarity to the subject, let's consider a mechanical professional within a company who has become paraplegic.

Since he will be unable to move or feel his legs, it is possible that he will be rehabilitated in the administrative sector of his company, as he "only" needs his upper limbs to work.

In this case, disability retirement is not granted.

A quadriplegic person who loses movement in their trunk, legs and arms cannot be relocated and will soon be entitled to this type of retirement.

Disability retirement requirements

In this sense, this benefit may be granted to an individual who meets the following requirements:

- Total and permanent incapacity proven by medical examination or by the public body in which he/she works, including information that rehabilitation in another position or job is impossible;

- Being working in the public service or contributing to social security at the time of the accident or illness (persons who are within the insured period are also accepted);

- 12-month grace period.

Therefore, there are 3 options so that the person does not need to prove the minimum requirement of 12 months, including:

Accidents of any nature, occupational accidents or illnesses, as well as an individual who has been affected by an illness specified in the list of the Ministry of Health, Labor and Social Security as a serious, disabling and irreversible illness.

Disability retirement due to illness

Check out the main illnesses that give you the right to this type of retirement:

| Severe nephropathy, advanced stage of Paget's disease (osteitis deformans) | Radiation contamination, based on the conclusion of specialized medicine. |

| Acquired immune deficiency syndrome (AIDS) | Ankylosing spondyloarthrosis |

| Severe heart disease | Mental alienation |

| Irreversible and disabling paralysis | Blindness or monocular vision |

| Parkinson's disease | Active tuberculosis |

| Multiple sclerosis | Leprosy |

| Malignant neoplasm | Severe liver disease |

Can disability retirement be canceled?

It is important for you to understand that disability retirement is not for life.

As mentioned above, it is a benefit aimed at those who have permanent and total incapacity for work functions.

However, there are cases in which the insured person is no longer incapacitated and can return to exercising his or her professional activity.

Therefore, re-evaluation through a medical examination is carried out every 2 years.

If a cure is confirmed, the benefit will be suspended.

Therefore, the expertise does not apply to the following groups:

- Insured persons over 60 years of age;

- Insured persons over 55 years of age and 15 years of receiving retirement benefits;

- HIV carriers.

For those who fit into any of the above groups and were still called for an expert assessment, it is important to seek the assistance of a social security lawyer.

Likewise, you cannot work while retired due to disability.

Although it is logical, not everyone follows the rule.

In other words, if it is reported that the retiree is working or has made any contributions to the INSS, the benefit will be cut.

Retirement by contribution time from A to Z

This type of retirement was the one that suffered the most changes due to the reform, however, it can still be granted in certain cases:

What is retirement based on length of service and how does it work?

Before the reform, the social security contributor only needed to prove the minimum time required in order to apply for retirement.

In addition, a requirement of 180 contributions was required.

Another possibility was the use of progressive points rules and proportional retirement.

Therefore, in the case of progressive points, it was necessary to reach a certain number to retire.

Therefore, age and contribution time were added together, with women needing 86 points to receive the benefit and men 96.

On the other hand, the proportional retirement had other requirements, such as a minimum age of 48 for women and 53 for men.

Another type of requirement would be a contribution period of 30 years for men and 25 years for women + additional time.

The social security factor was also mandatory in calculating proportional retirement.

And the benefit calculation was based on the highest salaries received between July 1994 and the date payments began.

Therefore, the lowest salaries were excluded from the calculation base in order to increase the retirement value.

However, the social security factor was applied to the calculation, thus reducing the value of the benefit for individuals who were younger and had a longer life expectancy.

Therefore, note that there were several rules, which in turn were capable of including several groups and guaranteed simpler access to retirement.

Why did retirement based on length of service end?

However, understand that this type of retirement was ended with the reform because the rules for granting it were changed.

Previously, it was possible to retire without a minimum age, something that is not possible today.

How do transition rules work?

But don't worry! You can still retire based on your contribution period through the transitional rules.

Thus, the first rule is the progressive age rule aimed at those who contributed to the INSS before the reform, but still have more than 2 years to go before retirement.

Therefore, it is necessary to meet the following requirements:

- Woman – 30 years of contribution, 56 years of age + 6 months per year, starting in 2020, until reaching 62 years of age;

- Man – 35 years of contribution, 61 years of age + 6 months per year, starting in 2020, until reaching 65 years of age.

Secondly, there is the 50% Toll rule, intended for those who had less than 2 years left to receive their retirement benefit when the reform came into effect.

That is, it is the only transition rule that maintains the social security factor.

In this sense, we can highlight the requirements:

- Woman – having contributed 28 years until the reform came into effect, and the additional period corresponding to 50% of the time that, on the date of entry of the reform, would be missing to reach 30 years of contribution;

- Man – contribution of 33 years until the Reform came into effect, and the additional period corresponding to 50% of the time that, on the date of entry of the reform, would be missing to reach 35 years of contribution.

For example, the reform arrived and you only needed 2 years to retire.

In this case, it is necessary to comply with 2 years + 1 year of toll, since 50% of the 2-year toll is equal to 1 year.

Transition rules – Toll 100%

Thirdly, there is the rule of Toll 100% which is optional and applies to both public servants and those who contributed to the INSS.

To be eligible, meet the following requirements:

- Woman – 57 years of age, 30 years of contributions, as well as completing the additional time corresponding to the period that, on the date the reform comes into effect, would be missing to reach 35 years of contributions;

- Man – 60 years of age, 35 years of contributions, as well as completing the additional time corresponding to the period that, on the date the reform comes into effect, would be missing to reach 35 years of contributions.

Therefore, if you opt for this transition rule and you only have 3 years left to retire before the reform, you must contribute for 3 years + 3, giving you a total of 6 years to obtain retirement.

Frequently asked questions

Check out the main questions on the topic below:

Retirement as an MEI, how does it work?

With the payment of the National Simple Collection Document for the Individual Microentrepreneur (DAS-MEI) and regularization by the Individual Microentrepreneur (MEI), there is the possibility of requesting various INSS benefits.

In other words, we can highlight sickness benefit, imprisonment benefit for family members, maternity pay and survivor's pension.

As for retirement, you are entitled to either disability or age-related benefits.

With DAS, the entrepreneur must contribute 5% to the INSS, guaranteeing the rights highlighted above.

And among the requirements, understand that it is necessary to contribute for at least 180 months, which is equivalent to 15 years.

Additionally, it is important to meet the minimum age requirement: 65 for men and 62 for women.

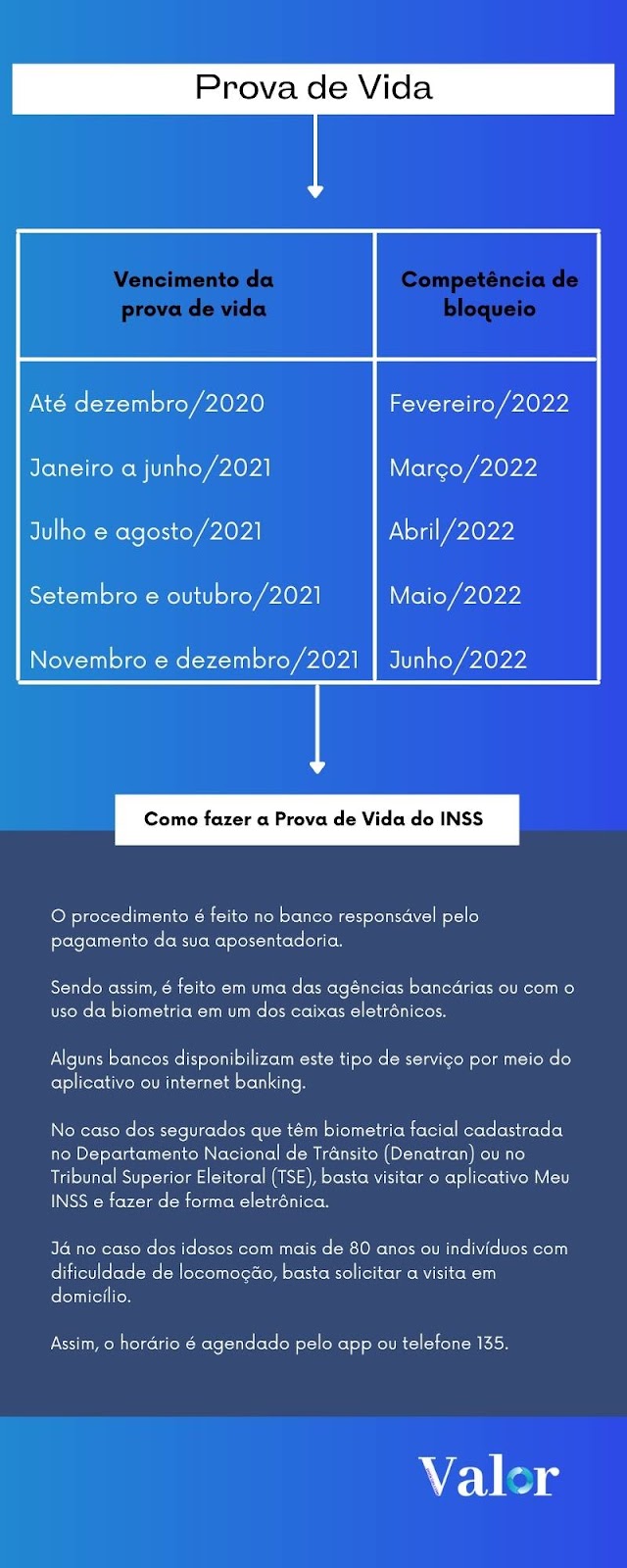

When does a retiree have to provide proof of life?

Attention: proof of life is now mandatory again, after a 3-month suspension.

This is a procedure carried out annually in order to maintain benefit payments.

From March 2020 to May 2021, the proof of life was suspended due to the Covid-19 pandemic.

Therefore, it was carried out again in July 2021, and with the worsening of the crisis, it was suspended again in October.

This year, around 3.3 million policyholders need to provide proof of life for 2021 between January and April.

Starting next month, retirements and pensions may be suspended if the procedure is not carried out.

According to an ordinance published on the 28th, in the Official Gazette of the Union, the deadlines for providing proof of life were extended and a calendar offered:

How can a retiree withdraw their FGTS?

After successfully retiring through the INSS, the insured can enjoy another benefit: full withdrawal of the FGTS.

In this sense, it is a benefit aimed at workers with a formal employment contract.

As a result, the most interesting thing is that even workers who requested the anniversary withdrawal can withdraw the remaining balance of the FGTS when they retire.

So, how do I request a withdrawal from the FGTS?

Therefore, present your CPF, identity document, proof of retirement and work card at one of the Caixa branches.

You can also request a withdrawal and inform your bank account through the FGTS app without having to leave your home.

When does a retiree receive his thirteenth salary?

Given that the INSS 13th salary was brought forward in the last two years, it is common to be anxious about when the benefit will be released in 2022.

In this way, through the Decree 10.410/20, new rules were established, with the first installment of the benefit being paid in August.

and the second installment will be paid in November.

Is retirement exempt from income tax?

No, in 2021 the second installment of the 13th salary had a different value due to the tax discount.

Therefore, taxation varies according to age:

That is, in the case of a retiree over 65 years of age, it is necessary to pay tax if their benefit is above R$$3,807.96.

For insured persons under 64 years of age, income tax is paid if they receive more than R$1,903.98.

Additionally, policyholders with certain illnesses can count on tax exemption.

Thus, we can highlight diseases such as:

Radiation contamination, Severe heart disease, Mental alienation, Blindness, Parkinson's disease, Ankylosing spondyloarthrosis, Multiple sclerosis, Leprosy, Advanced stages of Paget's disease, Severe nephropathy, Severe hepatopathy, Irreversible and disabling paralysis, Malignant neoplasm, AIDS and active tuberculosis.

In this sense, the request for an in-person medical examination in order to prove the illness and obtain tax exemption is made by the INSS website.

And another requirement is that the insured person aged 65 or over receives less than R$1,903.98.

Regarding the exemption request process, understand that it is necessary to send a series of documents to the Federal Revenue Service, proving the illness.

How does retirement work for those who have never worked?

You probably know a neighbor, relative or friend who managed to “retire” without ever having contributed to the INSS.

As we have highlighted throughout the content, people who do not contribute for the minimum period are not entitled to retirement.

But why does this happen?

Our country's Social Security system is contributory.

Therefore, it is essential to contribute so that in the future you will be entitled to receive insurance benefits.

For example, we can compare it to car insurance: only the customer who contracts and pays for the service on time can activate the insurance.

As a result, by becoming a contributor, you also become insured.

Therefore, we must clarify some situations in which an individual receives a benefit from the INSS even though they have not contributed:

This is the Continuous Benefit Payment (BPC/Loas) which guarantees a minimum wage.

To be eligible, you must be 65 years of age or older.

Furthermore, people with mental, physical, motor or intellectual disabilities who cannot support themselves financially also have the right.

In this case, a minimum age is not required, as long as the limitation prevents the person from having a full life in society.

So, other requirements are:

Have a family income of up to 1/4 of the current minimum wage, be a Brazilian national, not receive any other benefits and be registered in the Single Registry.

That is, understand that this is a social benefit and is not part of Social Security insurance, and is not seen as retirement.

Therefore, the person is not entitled to a survivor's pension or payment of the 13th salary from the INSS.

Therefore, it is correct to say that a person does not retire without contributing.

How does retirement work for those with low income?

According to Law No. 12,470, individuals without any employment relationship, without any income or with low income are entitled to retirement.

For example, housewives.

But, before highlighting this retirement, know that it differs from the Assistance Benefit for low-income people because it requires a contribution at a rate of 5% corresponding to a minimum wage.

Therefore, those who are registered with CadÚnico, do not carry out any paid activity, do not have their own income except Bolsa Família and have a monthly family income of up to 2 minimum wages can contribute as low income to the INSS.

The most interesting thing about making a contribution is that in addition to being able to count on retirement due to age or disability, you can check out other types of benefits.

For example, sickness benefit, imprisonment benefit, accident benefit, maternity pay and survivor's pension.

How does single contribution retirement work?

Remember the "one contribution miracle" rule we mentioned above? Well, let's clarify it below;

The rule improves the value of their insurance for individuals who contributed for at least 15 years up to July 1994.

This occurs because from this period onwards, the insured person does not have any benefit salary that is part of the average or if he does, he can discard it.

So, by making at least one contribution over the ceiling amount, you can retire with 60% on this contribution.

In other words, it is an excellent rule for those who started contributing between the 60s and 70s, and who after 1994 did not have good contributions to the INSS.

As a result, it is possible to increase retirement by almost 4 times through a single contribution over the ceiling.

However, to apply this rule, good pension planning is necessary, ensuring an analysis of the contributions made, the contribution period existing before July 1994 and the required period fulfilled.

Conclusion

Finally, in addition to Social Security, it is important that you know the details of Private Pension.

Therefore, also referred to as “private retirement”, this is an alternative for workers who want to guarantee a more comfortable future.