How to organize your fixed and variable accounts to avoid difficulties

How to organize your fixed and variable accounts to avoid difficulties!

Advertisements

Do you know how financial disorganization can cause chaos?

Having to deal with fines of up to 10% for late payments is a nightmare.

And that's not all, 85% of the population faces difficulties in paying their bills on time.

But how can we avoid this financial hardship that plagues so many people?

Managing your personal finances is crucial to your financial health.

With good planning, you can avoid overdrafts, which can have interest of up to 400% per year.

Let's see how to organize your fixed and variable accounts for a more peaceful financial life.

Main points

- 85% of the population faces difficulties in keeping their accounts up to date.

- THE effective financial planning can reduce late payment of bills by up to 40%.

- Using bill reminders helps reduce financial stress.

- The use of an overdraft can have annual interest of up to 400%.

- Creating an emergency fund is essential to mitigate financial contingencies.

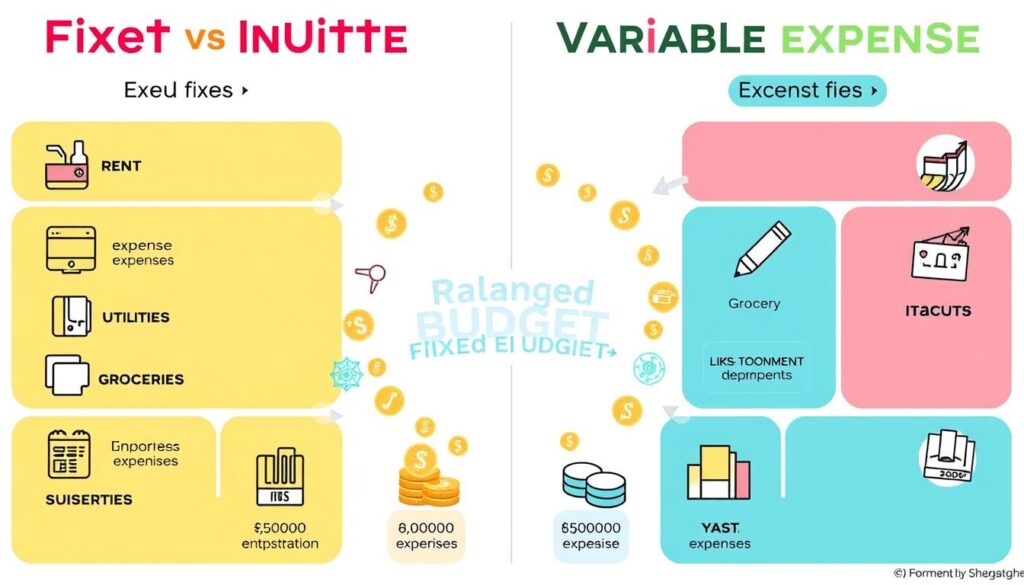

Understanding the difference between fixed and variable accounts

To control your expenses well, it is crucial to know the difference between fixed and variable expenses.

Fixed expenses are payments that don't change, like rent and health insurance.

They are essential for life at home and at work.

Important characteristics include being predictable and recurring.

On the other hand, variable expenses change according to what you buy or do.

Examples are electricity and water bills, and eating out.

These expenses are more flexible and can change or be cut when necessary.

The big difference is in the predictability of fixed expenses and in flexibility of the variables.

Fixed expenses are important commitments that cannot be ignored.

Variables can be adjusted to save money in difficult times.

| Fixed Expenses | Variable Expenses |

|---|---|

| Predictability | Oscillation |

| Regular Recurrence | Flexibleis |

| Essentials | Linked to Habits |

To take good care of your finances, it is important to categorize your expenses.

Distinguishing between fixed and variable assets helps to better understand the use of money.

This makes planning and financial decisions easier.

++ Which Expenses Are Deductible? A Guide for Individuals and Businesses

Creating a detailed budget

To be financially successful, it is crucial make a personal budget Well done.

A study by SPC Brasil shows that 461% of Brazilians do not prepare a budget.

This can make it very difficult to manage your finances.

The first step is to write down all your cash inflows.

This includes rent and investment income. It's also essential to record and categorize each expense.

This way, you better understand your financial situation.

Fixed expenses are things like rent and school fees.

The variables are expenses such as eating out and credit cards.

Keeping track of these expenses helps you see where your money is going and where you can save.

To better control your finances, it's a good idea to create custom categories.

This makes it easier to see where money is being spent and where savings can be made.

According to McKinsey, companies with a good financial sector cut their expenses by 29% in ten years.

To make a expense planning effective, it is important to define financial goals.

It is also essential to ask important questions, such as:

| Analysis Questions | Importance |

|---|---|

| Which expenses represent the largest part of the budget? | Identify areas for potential cost cutting |

| Should there be money left over at the end of the month? | Ensure a margin of financial safety |

| Do revenues cover expenses or do they require revision? | Assess the need for adjustments to planning |

Make a personal budget It may seem difficult, but it is essential to avoid debt.

This helps you achieve your financial goals.

THE financial control prevents debt and brings long-term economic stability.

Setting Financial Goals and Priorities

Define financial goals is essential to achieve your economic goals.

They serve as intermediate steps to achieving your big financial goals.

These goals can be divided into short, medium and long term.

To the financial goals short-term goals are achievable within 2 years.

For example, creating a emergency reserve from R$ 300 per month until accumulating R$ 5,000 is a strategic goal.

This helps cover unexpected expenses like car repairs or job loss.

For medium-term goals (2 to 5 years), investments such as debentures and equity funds are recommended.

An example is making a reservation of R$ 20 thousand to pay for a new car or R$ 10 thousand for a postgraduate degree.

To the financial goals long-term require financial discipline.

Investments that track inflation, such as stocks, are recommended.

A classic long-term goal is to buy your own home that costs R$1,000,000.

To define financial goals effectively, use the SMART methodology.

For example, investing R$ 150 per month can result in R$ 1,200 in 8 months, helping to pay off debt.

Keeping tight control of personal finances is crucial.

Use apps to effective financial management facilitates this process.

Diversifying investments is also important to increase your wealth.

In short, establish financial goals and clear priorities bring security in times of crisis.

They help achieve major economic goals by promoting a effective financial management.

++ Taxes in Practice: How to Choose the Best Tax Regime for Your Company

Organizing fixed and variable accounts: practical steps

To manage your expenses effectively, it's crucial to know how to organize fixed and variable accounts.

Fixed expenses are expenses that do not change and affect the budget in the long term.

Examples include rent, utility bills, and health insurance. It's important to pay these expenses on time to avoid interest and penalties.

Variable expenses, such as food and leisure, change in amount and frequency.

An example is the extra expense on food, which can exceed R$$100 per month.

Keeping a detailed record of these expenses helps you find ways to save money and avoid overspending.

To better understand the difference between these categories, see the table below:

| Fixed Expenses | Variable Expenses |

|---|---|

| Rent or real estate financing | Food (supermarket, restaurants, delivery) |

| Utility bills (water, electricity, internet and telephone) | Transportation (fuel, tickets) |

| Insurance (health, life, auto) | Entertainment and leisure (cinema, shows, travel) |

| Subscriptions and monthly fees (streaming, gyms) | Personal purchases (clothes, accessories) |

| Monthly debt and loan payments |

To make a spending adjustment effective, it is essential to keep a detailed record of all expenses.

Reviewing each category regularly helps keep your financial planning aligned with your goals.

Without planning, up to 70% of financial goals may be compromised.

Therefore, it is important to continually monitor and adjust expenses.

Tips to avoid unnecessary expenses and debts

To reduce unnecessary expenses, it is crucial to adopt savings strategies.

Without financial planning, debts can grow and affect your income.

Set clear goals for your spending, such as 15% for groceries, 10% for leisure, and 5% for clothing.

Late bills increase fees and interest costs, making it harder to save money.

Set aside a portion of your salary for annual expenses, such as property taxes and property tax.

Having an emergency fund is essential for unexpected events, such as health problems or repairs.

Improper use of credit cards and overdrafts can result in high interest rates, considered unnecessary expenses, and lead to indebtedness.

It is important to separate personal accounts from business accounts.

Use apps like GuiaBolso to identify unnecessary expenses.

Platforms like Contabilizei help with bank reconciliation.

Tracking fixed expenses helps you understand the cost of living and better plan your income.

Small daily expenses add up in the long run, affecting your budget.

Canceling unnecessary TV, cell phone, and streaming subscriptions improves your life.

Paying bills on time avoids interest and fines, which are unnecessary expenses.

Investing in financial education improves your financial situation.

Although statistics vary, using digital tools to manage finances improves personal management.

However, few people use these technologies.

++ 5 Steps to a Well-Planned Annual Budget

Organizing Fixed and Variable Accounts: Conclusion

To have a good financial health, it takes effort and planning.

It's important to know the difference between fixed expenses, like rent, and variable expenses, like food.

This way, you can manage your money better.

Adopt some saving tips can make a big difference.

For example, cutting fixed costs, such as bank fees.

Using financial software helps you better control and plan your finances.

It's essential to review your budget frequently. Do this at least twice a year.

This helps you keep your finances on track and achieve your goals.

Avoiding debt and having an emergency fund are also important steps.